Connect with Lenae

Your homeownership journey starts here. We'll help you every step of the way.

Apply NowAbout me

Explore more

Loan Options

Which mortgage is right for you? Check out our home loan options.

Check Out Loan Options

FAQs

Questions about your mortgage? Here are some answers to the most commonly asked questions.

Frequently Asked QuestionsConnect with Lenae

Your homeownership journey starts here. We'll help you every step of the way.

Apply Now

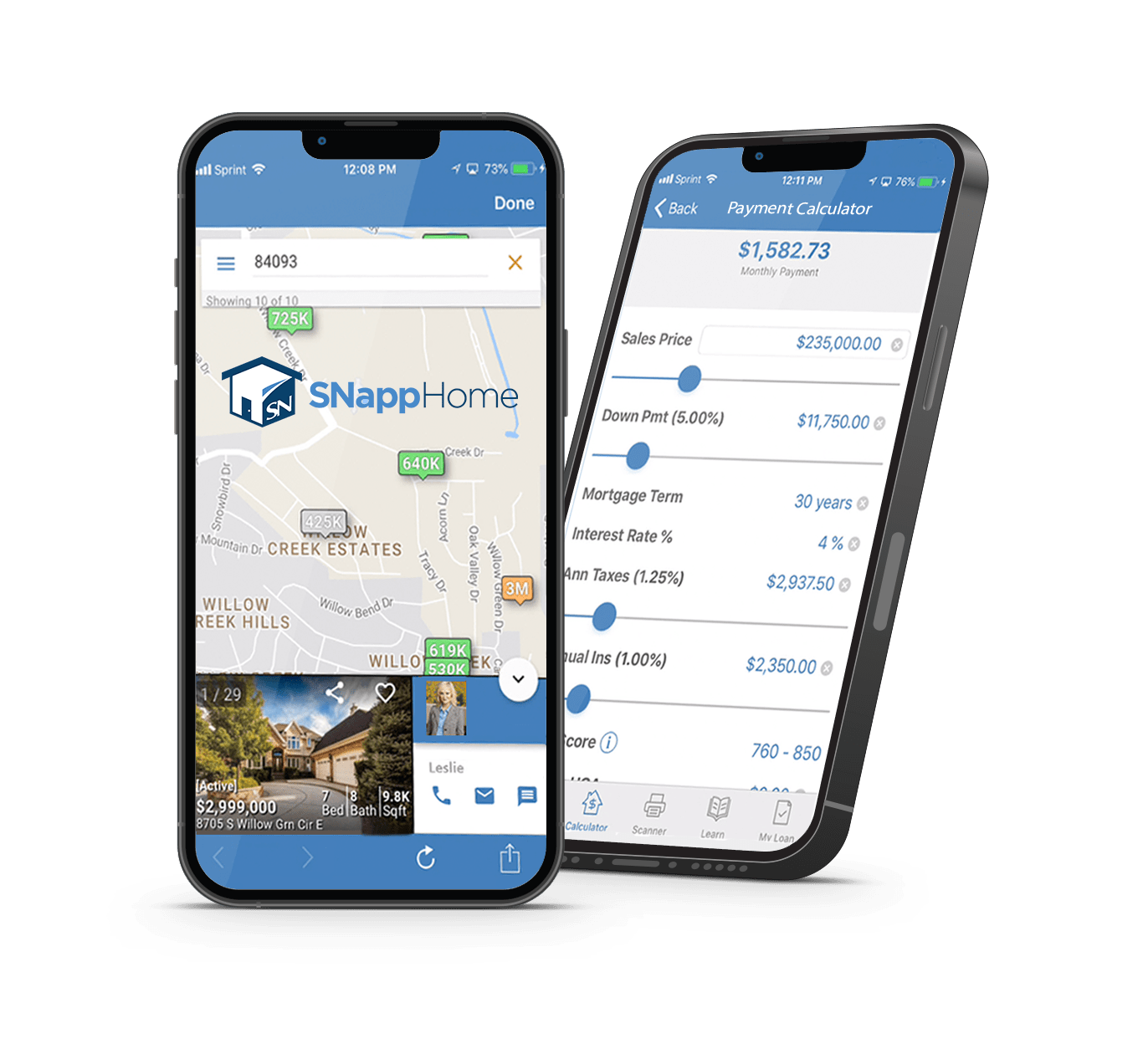

SNapp Mobile App

- Search for Homes

- Get Prequalified

- Payment Calculators

- Apply for a Loan

- Loan Options

- FAQs

- And More!

States Licensed In

- AR

- AZ 0945176

- CA DBO1521549

- CO 100537054

- FL LO106718

- GA 1521549

- ID MLO-2081521549

- IL 031.0074547

- IN 64467

- KY MC774221

- ME

- MI 1521549

- MN MLO-1521549

- MO 1521549

- NM

- NV 74123

- OR

- TN 1521549

- TX

- VA MLO-60972VA

- WY 104063

Mortgage calculator

Use our mortgage calculator to help you better understand your home financing options.

Lenae Meese

Mortgage Loan Officer

NMLS# 1521549

Your homeownership journey starts here. We'll help you every step of the way.

Apply NowReviews

Lenae Meese

Mortgage Loan Officer

NMLS# 1521549

Your homeownership journey starts here. We'll help you every step of the way.

Apply NowLenae Meese

Mortgage Loan Officer

NMLS# 1521549

Your homeownership journey starts here. We'll help you every step of the way.

Apply NowFAQs

What is pre-qualification?

Pre-qualification starts the loan process. Once a lender has gathered basic information about a borrower's income and debts, an opinion can be made as to how much the borrower should qualify for in purchasing a house. Since loan programs vary between credit, debt and down payment requirements, borrowers should get pre-qualified for each loan type they qualify for and are considering. Being pre-qualified is only a limited analysis and doesn't hold a lot of weight when it comes to negotiating a contract or reassuring a seller. There are many aspects to fully qualifying that could change a borrower's ability to qualify for a mortgage. Some of these things include: credit, length of employment, type of income, debt, liens or judgments, property type or condition, and other issues that come up during the approval process. Although it's tempting to start your home search before getting a pre-approval, we suggest you get that step completed sooner than later so you're armed with the knowledge of your real shopping budget and the power to negotiate the best deal.

What is a pre-approval?

Being pre-approved lets you know your price and term limitations, and therefore removes some of the stress of finding the perfect home. It happens after the lender has verified all information you've submitted in the application process. Being pre-approved also empowers you during the negotiation process. It gives the seller confidence in knowing your finances aren't an issue. You'll need a pre-approval to bid on a bank-owned or “short sale” home. Your offer won't even be considered if there are several offers on a home and you don't have a pre-approval.

Is there a cost to apply for a mortgage?

Generally, no — but occasionally the cost of a credit report will be charged. All other upfront fees, like an appraisal or application fee that may apply, will be disclosed to you as part of the application process and collected following your receipt of the early Truth-in-Lending disclosure and your approval to continue with the application.

How long will the loan process take?

Loan approval and funding time frames vary depending on the type of transaction and the complexity of your personal finances. The process can take as little as 10 days, and sometimes up to 45 days.

What is a lock-in rate?

The lock-in rate is the interest rate used to factor your monthly payment. The lock-in secures the interest rate during the process of your loan approval, as long as your loan is processed and closed prior to the rate expiration date. This date is given to you when you lock-in the rate.

When can I lock in my rate?

You can lock-in your interest rate once you have an accepted offer on a property. Your loan officer will discuss these options with you upon taking your loan application.

How long is my rate lock valid?

Depending on the type of transaction and the time you need, lock periods can be valid anywhere from 15 days to 180 days.

Should I refinance my mortgage?

Great question. There's a lot to consider when refinancing, and an SNMC loan professional can help you weigh this complex decision. Even a modest reduction in the interest rate can trim your monthly payment. The significance of such savings in any scenario will depend on your income, budget, loan amount, closing costs and the change in interest rate. An SNMC loan professional can help calculate the different scenarios for you, to determine if a refinance would be financially advantageous. Consulting your tax advisor is also encouraged, as your personal tax situation may affect your decision.

What documents will I receive at closing?

Start practicing that autograph! At closing, you'll be guided through a review of all the legal documents for the property you're purchasing or refinancing, and you'll sign each one. We'll give you copies of everything, and then it's all filed and recorded. We'll also make sure you get all pertinent information regarding your mortgage payment schedule, and servicing information for your new loan.

Can I still get a home mortgage if I've experienced credit challenges?

Obtaining a home loan is possible even with poor credit. If you have had credit problems in the past, a lender will consider you a risky borrower. To compensate for this added risk, the lender will charge you a higher interest rate and usually expect you to pay a higher down payment on your home purchase (typically 20-50% down). The worse your credit is, the more you can expect to pay for an interest rate and a down payment. Not all lenders choose to lend to risky borrowers, so you may have to contact several before finding one that will. Contact us to get an objective opinion on your credit and financial situation. Whether your situation calls for a short-term solution or a long-term strategy, we'll give you options to empower you to make an educated decision.

Lenae Meese

Mortgage Loan Officer

NMLS# 1521549

Your homeownership journey starts here. We'll help you every step of the way.

Apply Now